After years of rising borrowing costs that pushed millions of Americans out of the housing market, a long-awaited shift has finally arrived. Mortgage rates have fallen below 6% — a milestone many buyers and homeowners thought might take much longer to reach.

For families who paused their homeownership dreams and homeowners stuck with expensive loans, this sudden change is more than just a number. It signals a possible reopening of opportunities in a housing market that has felt frozen since interest rates surged after the pandemic.

But while the headline sounds like relief, experts say the story behind falling mortgage rates is far more complex — and its impact could reshape housing decisions throughout 2026.

A Major Milestone After Years of High Rates

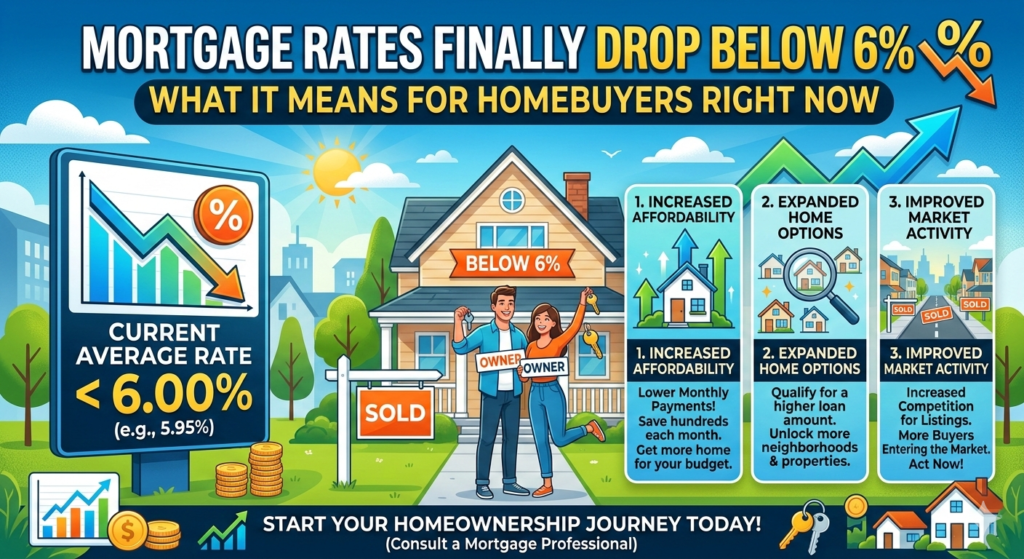

The average 30-year fixed mortgage rate recently slipped below the 6% mark, reaching its lowest level since 2022. This is significant because mortgage rates had climbed sharply over the past few years, at times nearing 8% as policymakers worked to control inflation.

Higher borrowing costs dramatically slowed home sales. Buyers struggled with affordability, while homeowners hesitated to sell because they didn’t want to give up low pandemic-era loans.

Now, the drop below 6% represents a psychological and financial turning point. Even small rate changes can significantly affect monthly payments, which explains why markets reacted quickly to the news.

Housing analysts say the shift could revive activity just as the traditionally busy spring home-buying season begins.

Why Mortgage Rates Are Finally Falling

Mortgage rates do not move randomly. They are influenced by broader economic forces, particularly inflation trends and expectations about future interest rates.

1. Inflation Is Gradually Cooling

Over the past year, inflation has shown signs of slowing compared with earlier peaks. When inflation eases, bond yields typically decline — and mortgage rates tend to follow.

2. Changing Expectations Around Interest Rates

Investors increasingly believe the Federal Reserve may pause or eventually reduce borrowing costs if economic growth slows. Mortgage lenders adjust rates based on these expectations even before official policy changes happen.

3. Economic Growth Is Moderating

Recent economic data suggests a cooling labor market and slower spending growth. While not signaling a recession, these trends reduce upward pressure on long-term interest rates.

Together, these factors have created conditions that allowed mortgage rates to move downward after years of steady increases.

What the Rate Drop Means for Homebuyers

For buyers, the difference between a 6.8% mortgage and a 5.9% mortgage can be substantial.

Lower rates reduce monthly payments, improving affordability at a time when home prices remain high. On a typical home loan, even a one-percentage-point decrease can save borrowers hundreds of dollars per month.

This increase in affordability also expands purchasing power. Buyers may qualify for larger loans or feel more comfortable entering competitive markets again.

Real estate agents are already reporting renewed interest from buyers who previously stepped back due to high costs. Many households had adopted a “wait and see” approach — and falling rates may finally bring them back.

Refinancing Activity Is Surging Again

Another immediate impact of lower mortgage rates is a revival in refinancing.

Homeowners who purchased properties during high-rate periods in 2023 and 2024 now have an opportunity to replace expensive loans with more affordable ones. Lower payments can free up cash for everyday expenses, savings, or debt reduction.

Mortgage lenders have reported a noticeable increase in refinancing applications as borrowers rush to take advantage of improved conditions.

However, refinancing demand still faces limits. Millions of homeowners secured ultra-low mortgage rates below 4% during the pandemic years. For them, today’s rates — even below 6% — may not yet justify refinancing.

The “Lock-In Effect” Still Shapes the Market

One of the biggest challenges facing the housing market today is what economists call the “lock-in effect.”

Homeowners with very low mortgage rates are reluctant to sell because moving would mean taking on a higher interest rate. This reduces the number of homes available for sale, keeping inventory tight.

Even as mortgage rates decline, housing supply remains limited. Fewer listings mean prices stay elevated, which continues to challenge first-time buyers.

Experts say this dynamic explains why falling rates alone cannot instantly solve affordability problems.

Home Prices Remain a Major Obstacle

Although borrowing costs are improving, home prices remain historically high due to years of underbuilding and strong demand.

Limited housing construction combined with population growth has created a persistent shortage of available homes in many regions. As a result, lower mortgage rates may actually increase competition among buyers, potentially pushing prices higher again.

This creates a delicate balance: falling rates improve affordability, but rising demand could offset some of those gains.

For first-time buyers especially, saving for a down payment remains one of the biggest hurdles.

Experts Say Psychology Plays a Huge Role

Interestingly, economists believe the emotional impact of crossing below 6% may be just as important as the financial benefit.

Consumers often react strongly to milestone numbers. Mortgage rates starting with a “5” feel significantly more manageable than those above 6%, even if the monthly difference is modest.

When buyers believe conditions are improving, market activity tends to accelerate. Increased confidence can lead to more home tours, more offers, and eventually more completed sales.

Some analysts describe this moment as a “confidence reset” for the housing market after years of uncertainty.

What Experts Expect for Mortgage Rates in 2026

While the recent decline is encouraging, most forecasts suggest mortgage rates will remain volatile.

Economists expect rates to fluctuate within a moderate range rather than fall sharply. Inflation risks, global economic conditions, and Federal Reserve decisions will continue influencing borrowing costs.

Current projections suggest:

- Rates may hover between 6% and 6.4% through much of 2026.

- Temporary dips below 6% could occur during favorable economic periods.

- A return to pandemic-era rates near 3% is highly unlikely in the near future.

This means buyers waiting for extremely low rates may end up waiting indefinitely.

Why This Story Matters Beyond Real Estate

Mortgage rates affect far more than home purchases. Housing plays a central role in the broader economy.

Lower rates can stimulate:

- Home construction and renovation activity

- Consumer spending tied to homeownership

- Banking and lending growth

- Job creation across multiple industries

When housing activity improves, related sectors — including furniture, appliances, and home improvement — often see increased demand.

Because of this, economists closely monitor mortgage trends as an indicator of overall economic health.

Advice for Buyers and Homeowners Right Now

Financial experts caution against trying to perfectly time interest rate movements.

Instead, they recommend focusing on personal financial readiness:

- Buy a home when monthly payments comfortably fit your budget.

- Compare loan offers from multiple lenders.

- Consider refinancing if savings outweigh closing costs.

- Remember refinancing can always be done later if rates fall further.

Housing decisions should be based on long-term affordability rather than short-term market predictions.

A Market Slowly Moving Toward Balance

The U.S. housing market has spent several years adjusting to higher borrowing costs and changing economic conditions. The drop below 6% does not instantly solve all challenges, but it signals progress toward stability.

Lower rates may gradually encourage more buyers to enter the market while giving homeowners financial relief through refinancing.

If rates remain relatively stable through the year, housing activity could steadily improve rather than surge dramatically.

Relief Arrives — But Caution Remains

Mortgage rates falling below 6% mark an important turning point after years of financial pressure on homebuyers and homeowners. The change is already boosting confidence, increasing refinancing activity, and drawing buyers back into the market.

Yet challenges remain. High home prices, limited inventory, and economic uncertainty continue shaping the housing landscape.

The key takeaway is simple: the housing market is not returning to the ultra-cheap borrowing era of the past, but it may finally be entering a more balanced phase. For many Americans, 2026 could represent the first realistic opportunity in years to reconsider buying, selling, or refinancing — provided decisions are guided by long-term financial stability rather than short-term excitement.

⭐ Key Highlights

- Mortgage rates dropped below 6% for the first time since 2022

- Lower borrowing costs are improving affordability for buyers

- Refinancing applications are rising as homeowners seek savings

- Housing inventory remains tight due to the “lock-in effect”

- Experts expect rates to fluctuate but stay near current levels in 2026

- Falling rates could gradually revive housing market activity

Related Article

What Cancer Does Bhad Bhabie Have? The Truth Behind the Blood Cancer Reports Explained

Mumford & Sons Take Over SNL Tonight — Start Time, Host Reveal, and What Fans Didn’t Expect

Think You Know the News? The CNN News Quiz Is Challenging Millions — Can You Score High?

4 thoughts on “Mortgage Rates Finally Drop Below 6% — What It Means for Homebuyers Right Now”